Follow CTR and Casual Talk Radio:

Website: https://www.CasualTalkRadio.net

Twitter: @CasualTalkRadio

Facebook: @ThisIsCTR

[00:00:04] You're listening to Casual Talk Radio, where common sense is still the norm. Whether you're a new or a longtime listener,

[00:00:12] we appreciate you joining us today. Visit us at CasualTalkRadio.net. And now, here's your host, Lyster.

[00:00:21] Welcome welcome, and if I come across as a little bit gravelly, I apologize.

[00:00:26] I think allergies are just kicking my tail right now because you know, we're in May,

[00:00:30] and I think allergies are just kind of starting to take over. I don't know for sure, but it certainly

[00:00:37] feels like it. It doesn't feel normal or natural for me. CasualTalkRadio.net welcomes you back

[00:00:43] or welcomes you to the show. My name is Lyster. I am your host, and I've got a couple of things

[00:00:48] that I wanted to follow up on. So I did a couple of episodes so far about the journey

[00:00:56] to buy a home. And it seemed like these are popular episodes. The information shared seems

[00:01:00] to be of value to some people. But it occurred to me that you may have heard me, if you've

[00:01:05] listened for a while, make certain statements that might have caused you to scratch your head.

[00:01:10] And I figured, why don't I elaborate on what I mean? Because I need to make sure that it's clear

[00:01:16] and why I'm not trying to be, you know, a naysayer or anything. By no means am I, but I think I

[00:01:24] think I need to clarify terms. So with buying a home, it ties to buying a home. Buying the

[00:01:31] home involves largely three things. So be sure to take notes. I don't mean on your phone,

[00:01:37] but be sure to take notes on this. Number one, most importantly, when buying a home,

[00:01:42] money, obviously, right? You need money. The key is it's not just the money that you have.

[00:01:50] It's also the money that you expect to make. It's the money that you've made in the past and

[00:01:56] the source of that money. It's where the money is right now. It's making sure that you're

[00:02:01] going to have enough money come closing time. Money kind of drives largely the conversation,

[00:02:07] but it's not the only thing to think about. It's just the top of the list. The second,

[00:02:12] credit, right? Credit is less important. It's not that it's not important. I'm saying it's

[00:02:18] less important than money. What do I mean? You'll notice and or may not even know,

[00:02:25] but many wealthy people have terrible credit. The reason is because credit's a scam. And

[00:02:32] you've heard me talk about that. That is going to be the topic of my conversation here today

[00:02:37] I'll get back to it. Number three, location. You hear it. Location, location, location. Well,

[00:02:44] what does that mean? Well, some markets are easier to buy than others. Some markets are

[00:02:50] easier to sell than others. Some markets have crime considerations. Some markets

[00:02:56] have terrible schools. Some markets have lending programs that are designed to help you buy a

[00:03:01] home. Some markets have junk homes like Chicago. Some markets have more foreclosures than others.

[00:03:07] Some markets limit who can buy. Did you know some markets actually have covenants in the

[00:03:14] neighborhoods written in the actual documents, in the bylaws that prohibit certain people from

[00:03:19] purchasing homes? So if you're let's say Native American descent, let's say you're Asian

[00:03:25] American descent, let's say you're Hispanic American, let's say you're Black American,

[00:03:29] regardless. If you're not white American, in some places they actually wrote in laws and bylaws

[00:03:36] and covenants and any document they could justify prohibiting you from purchasing home

[00:03:42] or from holding property. I should be more clear. It's not even about the purchase.

[00:03:46] It's about are you the owner of the property that's not allowed? Are you here

[00:03:51] because you're a slave? Well, we'll let that slide. So location matters. Sometimes you

[00:03:58] might want to live in a certain place because you're close to family. Sometimes you want to

[00:04:02] live in a certain place because of military connects. Sometimes you want to live in a

[00:04:06] place because it just appeals to you and your personal sensibilities or sometimes you're

[00:04:12] looking at it from safety measures or good schools or something, but usually it's my job

[00:04:18] uprooted and went somewhere else. I had a situation where a company I worked for was

[00:04:23] based out of Southern California and I had, I'm pretty sure I had long left by this point,

[00:04:30] but they uprooted and went to Nevada and they offered everybody basically a year's worth of

[00:04:36] pay if you wanted to come along. The vast majority of people didn't want to go because

[00:04:40] it's Nevada and so many of those people loved California for reasons I will not understand,

[00:04:44] but they offer people a thousand, you know, basically a year's worth of pay to uproot and

[00:04:50] move. And then that company is still out there as far as I know, but that may be your

[00:04:55] justification for why people move is their job took them. That's rare, but it does happen.

[00:05:00] It's most commonly military proximity to family more commonly or cost. These are usually the

[00:05:08] three. Why did Leister decide to move? And I've moved a lot. So the journey started in

[00:05:15] California. It went to Washington state. I don't regret the move to Washington state,

[00:05:22] but Washington state Western Washington state should be clear is a cesspool terrible place

[00:05:28] unless you can work from home. I should be, I need to be emphasizing that if you can work

[00:05:34] from home, I think there's great places in Washington state, the Tri-Cities, the far

[00:05:40] western side, Blaine up North. There's really nice, what is it? Bellingham. I believe it is.

[00:05:46] There's really nice places in Washington state. If you can work from home, it's when you cannot

[00:05:52] work from home that it's a cesspool piece of garbage to live in. And unfortunately I was

[00:05:57] working for an organization that didn't let me work from home. And then by the time I,

[00:06:01] because I assumed I was going to be there a while I got settled. I bought a home up there.

[00:06:07] I think I told the story about a house up there. I regret the house I chose, not the experience,

[00:06:12] but then the one person who was my advocate at the company retired rather suddenly. So now I

[00:06:18] can't stand hardly anybody I work with, but I'm stuck with this house that I just bought.

[00:06:23] I found another opportunity consulting, but I was working for somebody else. So I'm beholden

[00:06:29] to their rules and I'm, I own this house that I got to pay for. Then I got scammed with

[00:06:34] a state program, which goes back to the whole money thing. The state program is for people who

[00:06:40] don't have enough to put 20% down, which I didn't at the time. And I could have saved it,

[00:06:46] but to do so would have taken me a long time because the town home I was in raised the rent

[00:06:53] from 1500 bucks a month to just over $2,200. And I told them to GFY as Elon Muslite said.

[00:07:00] So I ended up buying the home, which again, I couldn't have known that the person my advocate

[00:07:06] was going to retire. Couldn't have known that time outside of the fact that I had to go into

[00:07:11] an office. I wouldn't have minded if I could have worked from home, it'd have been perfectly

[00:07:16] fine. So when I got this consulting gig and it's work from home, I'm excited because I

[00:07:20] figure I'll be there for a while. And then I can build up enough money to eventually live

[00:07:25] where I really wanted to live. Well, that consulting, cause I'm working for somebody else

[00:07:28] now. They're trying to ship me all over the nation. I was never actually home. So I'm paying for

[00:07:34] this amazing house that's 2,600 square feet. And I'm never there because I'm constantly on a

[00:07:39] plane flying from location to location out of pocket upfront. So it's a reimburse model.

[00:07:45] And it takes basically two weeks to get your money back while they fly you two weeks at

[00:07:49] a time. I'm a tall dude, so I'm not sitting in sardine seats. I'm having to do first class.

[00:07:55] And so, you know, your, and then hotels, especially when I went to Boston, sometimes it's 2000 bucks

[00:08:01] minimum for the trip. And it builds up. So I don't have a lot of money discretionary

[00:08:08] for this. And then all sorts of stuff happened. I get into another one. That one is it's essentially

[00:08:13] a consulting, but I'm full time. And that was a nightmare because although I have a

[00:08:18] American express corporate car with no credit limit, they allowed the customer to dictate

[00:08:22] how much I can spend on it. And the customer was allowed to dictate what hotels you stayed at

[00:08:27] to control the spent the spin down to the dollar, which wasn't going to work. So

[00:08:34] I have to leave these and I get a different opportunity. So now my next journey is

[00:08:38] Colorado. This is the fiasco that was, and that was my fault because I was,

[00:08:44] I wanted to get settled and I didn't realize what I was walking into story behind that is

[00:08:51] I get the situation presented to me. It was actually full time, but came through an agency.

[00:08:57] So I do the presentation. They flew me up there the whole nine. I like it.

[00:09:03] Certainly wanted to be out of Washington. Great. I accept it. They're told that I'm telling

[00:09:08] me you're going to run the show. I get in. They had already started down the wrong path.

[00:09:13] So then I had to course correct. And unfortunately I lost track of it because

[00:09:17] there was so much to do because they had gone so far wrong. I lost track of it. So

[00:09:22] my car was left at the parking, the airport parking for countless months. I think I didn't

[00:09:27] get it back. I want to say it had to be like two or three months. It was, it was a while

[00:09:33] that it was sitting at the parking. So I'm paying for it. The meter's right.

[00:09:36] So I finally go get my car. Now I got to drive my car up there. And unfortunately,

[00:09:42] because of the situation with the house and I'm not going to give over specifics,

[00:09:44] but suffice to say I misunderstood that you hauls you box was a piece of crap. That's my fault.

[00:09:53] I should have understood how bad they were because I had a situation with them before

[00:09:57] and I didn't think it through. So they don't for you, FYI, they don't allow you to do same

[00:10:03] day drop off and pick up of the crate like you pack does ABF. So there was a fiasco trying

[00:10:11] to get all my stuff packed in there, all of my critical things. And it's just me and I got to get

[00:10:16] back to work because it's only over a weekend. Only got the two days. And there was other stuff

[00:10:21] happening with the house. So I didn't get all my stuff. So I lost a lot of paperwork from

[00:10:26] like my video game business and some old tax stuff that I don't really need, but it was

[00:10:29] nice to have it. I lost a lot of that critical paperwork. I lost my whole stereo

[00:10:34] setup that I had. I lost my, I kept one of the blankets, but it wasn't the good one.

[00:10:40] I lost a lot of valuable things. Nothing that was critical, nothing that I could do without.

[00:10:47] But I lost a lot of stuff that I probably shouldn't simply because I misinterpreted

[00:10:52] U-Box with U-Haul and I overestimated how jacked up it was going to be when I got to Colorado.

[00:11:01] So fine. I finally do that and I had to let stuff go and it was what it was. And then I get

[00:11:06] to Colorado. I had to shack up in an executive place situation rental because although I was

[00:11:13] going to make good money, it wasn't the money I really wanted yet. I think only started at like

[00:11:19] 86,000 bucks or something. It wasn't that high. And I know some people are listening like,

[00:11:23] geez, are you crazy? It wasn't that high because I was already making

[00:11:27] 80 something thousand dollars at the previous. So for me, relatively speaking,

[00:11:32] it wasn't a significant enough increase. I got to the point that I wanted, but it took

[00:11:38] some, it took some years to get to that point. So now I'm in Colorado. I rented the entire

[00:11:43] time I was in Colorado. I was never at a point comfortable of buying a home mostly for

[00:11:48] credit reasons. That's why I said it ties back when I talk about credit and why it's a scam.

[00:11:52] It was mostly credit reasons. Now for renting credit was perfectly fine. I never had a

[00:11:58] problem renting anything based on credit and out there they didn't care about references,

[00:12:03] which was really good because I don't do references. I think it's stupid

[00:12:07] because people just lie. They just call a buddy and say act like a reference. You can't prove it.

[00:12:12] So it's a waste of time. We know everybody frauds the system. That's why I think it's

[00:12:16] stupid. Go off the credit if you have to. I think that's stupid because you're not letting

[00:12:20] me money. So now I'm trusting, I'm telling the story about how it's a scam in Colorado.

[00:12:27] I didn't have to deal with those reasons why it's a scam, which was one nice thing about Colorado.

[00:12:33] However, I started a new boss came in. I started having issues with this Joker because he doesn't

[00:12:38] understand and he's bowing down to the client. The client, they don't know any better

[00:12:42] because somebody prior to me had screwed up and they don't get it. And so it's a chaotic

[00:12:47] mess. And I was making significant progress. I was having fun doing it and I thought it was

[00:12:51] good. But at the same time, there's stuff that I'm not cool with. So I decide I'm going to leave.

[00:12:57] I gave the guy warning and he laughed in my face. All right, cool. I'll show you. And I

[00:13:01] decided to leave. So then that was the mistake I made to go to Oregon now. And I accepted

[00:13:08] that when they flew me out again. I should have known something was up when I went out

[00:13:13] for the interview because when I, this is full-time, because when I flew out there,

[00:13:18] there's a hotel that's like walking distance from the place. And I got there late night. It

[00:13:24] was like 11 o'clock or something. I still have my jacket on because it's rainy, it's cold.

[00:13:28] I had my hat on and the lady behind the counter, I told the story, my things up on Yelp

[00:13:34] still, the lady swore she couldn't find my reservation that the place had set up for me.

[00:13:41] And I even gave her, I offered her the number, look it up by the number. I guarantee

[00:13:45] you it's there. And she swore she couldn't find it by my name. She couldn't find it by anything

[00:13:49] at all. So now I had to go down to, I'm pretty sure it was Howard Johnson. I don't know if

[00:13:55] anybody stayed at Howard Johnson. Howard Johnson does not make you feel at home unless you

[00:14:00] live in a slum because Howard Johnson is the worst, slummiest, radiest, other than Travelodge,

[00:14:07] radiest hotel I've ever stayed in in this business. But I have no choice because I didn't

[00:14:12] carry significant money on me or in the banks. I just didn't. So that was the only place I could

[00:14:18] go because it was like 40 bucks a night. So I go down to the Howard, it's down the road,

[00:14:22] I go to the Howard Johnson, I stay there, the toilet's tiny, it's noisy, it's dirty.

[00:14:28] I didn't see any insects but it was horrible and I could tell that some sort of sexual

[00:14:33] activity was going on. So I do the Howard Johnson business and then the next day

[00:14:38] I go to the place to do the interview because it was like a Sunday night. Now Monday I go to the

[00:14:42] place and I tell them, they're waiting for me because they don't know where I was because

[00:14:48] they tried to call the hotel to check on me and I wasn't there. The other hotel, I get there

[00:14:53] and I'm telling them, they swore they couldn't find the freaking thing, sorry, and then you

[00:14:57] guys are closed on Sunday so there was nothing I could do. Apparently they talked to the other

[00:15:01] hotel and they apologized profusely because they were trying to search against my last name

[00:15:07] as the first name. Now I gave her the appointment number so I know the excuse was a bunch of crap,

[00:15:13] that's number one. Number two, I specifically said, I'm pretty darn sure there was not anybody

[00:15:20] else there that had my name as their first name. If you take the time to look,

[00:15:26] I'm guaranteeing you it was not the case. I know she's lying, I know she's lying. What

[00:15:32] happened, I can guarantee you and it seems like it's a pattern in some places. They saw,

[00:15:36] I'm sorry, a black American wearing a black coat and a black hat and they profiled me.

[00:15:42] That's what happened. She profiled me as if I don't belong there and this is a high end

[00:15:47] swank, you know, like a $300 a night hotel. This was not a simple hotel. That's how I know

[00:15:53] that's what it was. They tried to offer me, okay you can go get some meal and it's 10 bucks

[00:15:59] off. I'm like, no you're going to do the meal for free, you're going to do the room for free or

[00:16:03] screw you. They finally said well we're sorry and we'll give you the room and this and that

[00:16:09] and the other and I actually, I'm pretty sure I said I'll do the last night just because I'm

[00:16:15] not going back to the Howard Johnson but I'm just doing the one. I'm not going to stay

[00:16:21] longer than I need to. I don't want your dinner, I don't want none of that because

[00:16:24] you're just going to profile me at the dinner counter and they got all pissed off and it's

[00:16:27] like look bro sorry your lady profiled me. That's what happened. It's the only logical

[00:16:32] explanation because she couldn't, you're telling me you couldn't find it by a reservation number

[00:16:37] that means you didn't try. It's not possible. The reservation number takes you straight to the

[00:16:41] thing so if you didn't just check and I even gave her my driver's license the whole nine

[00:16:47] she didn't check, she didn't bother. That's what I'm saying is it can only be profiling

[00:16:51] because there's no way with a reservation number you're not finding it so I don't want

[00:16:56] anything to do with them. They're apologizing all that when I got there I wasn't trying to hear this

[00:17:00] but that incident should have told me this is, this isn't going to work and the phone call I

[00:17:06] had with the manager he lied because he said nope you're reporting to me and this is what

[00:17:11] I need and as long as you do that we're all good and I get in there so I accepted the

[00:17:15] position and I remember during the interview asking him I'm struggling to understand how I

[00:17:20] can help. I'm struggling to understand what you need and he said they're screwing up

[00:17:25] in another department we need somebody to get it done right because our customers are pissed off

[00:17:29] essentially is what he said and your role is designed to come in here and make sure our

[00:17:34] customers are getting what they need. Okay I treat that as authority, I treat that as you're

[00:17:38] going to give me some authority and autonomy to do it right. That means whoever's over there

[00:17:42] they're gonna have to follow my instructions and he's like yes that's what we need we need

[00:17:46] it done because they are they are the customer we got to take care of them. Okay I'm cool with

[00:17:52] that the money was good I didn't ask for too much money it was the same it was actually less

[00:17:57] than I was making before but it was my threshold at the time full time and then Oregon has certain

[00:18:03] tax benefits that made it you know seem like a worthwhile and then rent wasn't that high.

[00:18:07] Now there were other issues but the point is the money seemed to make sense so I accept

[00:18:10] the offer I get up in there and he's telling me again now here's where it's shifted all

[00:18:16] of a sudden I'm reporting to this other chick and I'll call her a chick because I

[00:18:20] couldn't stand her. I'm reporting to this other chick and I don't even know who this

[00:18:24] I think she was in the interview and I just didn't put two and two together I thought she

[00:18:27] was just some lowly worker but apparently she's the soup of this group and I'm reporting into

[00:18:32] her that wasn't what we agreed and I really don't like her you know she's a black American

[00:18:39] or at least mixed so I'm assuming there's something there but again this was not

[00:18:43] disclosed to me beforehand and she never interviewed me as a boss so I could get a

[00:18:49] chance to assess her ability to lead so I didn't know she was capable or competent to

[00:18:54] be able to lead somebody with my energy turns out she couldn't. Okay he's emphasizing again

[00:19:02] no what we talked about is what it is meet with them let's get this thing going.

[00:19:07] Now this is a new setup that this hasn't happened this is just whatever I get in and

[00:19:14] instinctively they're all put not all mostly it's one person but there's resistance because

[00:19:20] they weren't told I was coming in and they weren't told what my role was going to be

[00:19:24] so they're pushing back naturally because they don't know what the hell's going on

[00:19:27] I'm telling them my boss hey they don't they don't seem to want my help here I'm sitting

[00:19:31] in rooms wasting time this organization has mandatory furloughs in their case pretty much

[00:19:39] it was like every other week or something else there's a mandatory furlough day forcing you to

[00:19:45] go unpaid even though it's like wait a minute I'm ready to work I'm salaried you can't do that

[00:19:51] by law FLSA if I was ready to work and I worked at least an hour that week you will pay

[00:19:57] me the full week and they were essentially violating the law and willing nobody's questioning

[00:20:01] this business okay that's not going to work they won't let you work from home everybody else

[00:20:08] started six I'm trying to start at eight because I'm not waking up at six out here

[00:20:13] they won't let me dial in you know to say I'll just dial in if your meetings at seven o'clock

[00:20:17] I'll just call in they wouldn't let me do that even though all we're doing is talking

[00:20:21] about what did you do I didn't do anything because you're not letting me so it's a waste

[00:20:25] of time I don't need to be in the room back and forth the place I rented and this will

[00:20:30] freak some people out and that's okay that's what I want so the place I rented looks nice

[00:20:35] on the surface but then sometime and I want to say this was I want to say it started in summertime

[00:20:42] there were these little brown I say little spiders that started coming in through the cracks

[00:20:48] of different doors it had a major ant problem like I've never seen ants to that degree before

[00:20:55] but the spiders I actually have pictures of these things I might even do it on the on the

[00:21:00] thumbnail if I can track it down but there are these these little brown spiders I want to say

[00:21:05] they're like quarter size so I say little I'm not I don't they're little in you know retrospect

[00:21:12] but they're like quarter sized spiders that are coming into the cracks of the door and there's a

[00:21:18] lot of them there's a lot of them I had to think there was at least six or seven that I

[00:21:24] found purposely and killed in this business so it's got pest issues it's got the ant issues

[00:21:31] the neighbor upstairs it's like two guys and they were constantly arguing late night this

[00:21:37] one guy's yelling at the top of his lungs and he sounds like he's slow or somehow I don't know

[00:21:44] what going on but that so there's that so I can't really sleep because of this business

[00:21:49] you got the ant issues you got the spider issues there's no air conditioning in it

[00:21:53] so that's a problem it's hot as all get out I had to get a you can't put a window AC

[00:21:58] so I didn't know all this stuff right when I'm winning this so I got that I can't work from

[00:22:02] home like I think I should be able to do I've got a soup who's incompetent I got this manager

[00:22:07] who lied I got this group who's screwing up but they won't let me fix it and I'm essentially

[00:22:13] collecting a check doing nothing okay that's cool I'm getting money but I need to be

[00:22:18] engaged I need to be doing something and I certainly need to be satisfied where I'm living

[00:22:22] and what I'm doing and there's a taco shop but it's kind of crap like it's getting bad food

[00:22:28] ratings there's everything shutting down it's kind of like a slum area I'm just not happy so

[00:22:33] I was only there I was only there from that January all the way through at this point

[00:22:39] August officially but I formally moved in like October ish yeah October is when I formally

[00:22:50] moved I was still renting it but I finally moved that's where I headed to Nevada and I only went

[00:22:54] to Nevada because my client is in California at the time when I left this other place so I left

[00:23:00] that place in April because of the joke that was going on and went and became a consultant

[00:23:06] my own business so that's what started by journey of being my own working for myself making

[00:23:11] my own money and then I ended up in Nevada to be close to the client and get away from all this

[00:23:15] garbage as so then COVID hits right COVID that what COVID taught me is it absolutely doesn't your

[00:23:25] credit just simply doesn't matter as much as it used to it's all about the money not just the

[00:23:31] money you have but the money you can produce and money you can prove it doesn't mean that

[00:23:36] it's a guarantee sure bet because a lot of people who are renting they they are coming

[00:23:41] they're renting because the credit's not enough to purchase however I want to tell

[00:23:45] I want to school you on a couple things did you know that in some states not all but in

[00:23:50] some states it's actually easier to buy something than it is to rent did you know

[00:23:58] that depending on how much money you can produce and you can prove you probably could

[00:24:03] buy something you know something simple like a condo or something that would result in

[00:24:08] a monthly payment that could be half of what you pay in rent do you know why what I'm saying is

[00:24:15] you can prove this you can go and look yourself do you know why I'm so confident in it

[00:24:20] and you heard me say about the 20% even counting not doing 20% the reason is because

[00:24:26] the loan programs they want your money the banks want your money the FHA needs your money

[00:24:33] and so they're willing to come down on the credit requirements and they're less picky about

[00:24:38] the minutia of what your credit says so in other words let's say you work with a local bank let's

[00:24:45] say you work I don't know what banks you have local but whatever local bank that's not like

[00:24:48] a bank of America I'm talking to your regular community banks or a crediting or something

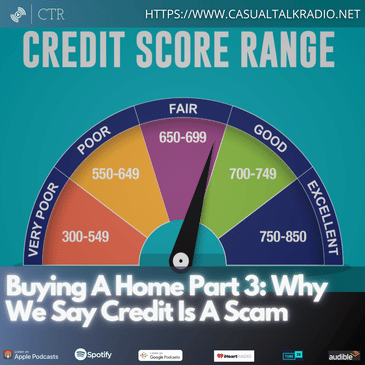

[00:24:53] they're going to check your credit scores primarily they're going to look at the credit

[00:24:58] score and look for a number that's 620 or greater on your score I've heard people and

[00:25:05] I've worked at credit bureaus this is why I know this is the case I've talked to people

[00:25:09] who swore up and down that their credit score was in the low 400s and I'll tell you from

[00:25:16] life experience I struggle to understand how that's even fucking possible because I've gone

[00:25:22] through a lot I've gone through a lot and I'm talking even before when I was in California

[00:25:30] I've gone through a lot to where I didn't know any better because I was younger

[00:25:36] to damage my credit and I'm pretty sure my credit score never went lower than 590 so when

[00:25:42] people tell me that they had a credit score in the fours I don't even know how it's possible

[00:25:48] unless if you had you know like liens or something you know tax liens or people talk

[00:25:54] about medical bills even medical bills wouldn't do too much of this so I know there's people out

[00:25:59] there that have extremely low credit scores and I struggle to understand why it is but most

[00:26:05] people are at least 620 let's say six to six twenty most people are at least this on a loan

[00:26:13] for a mortgage 620 is kind of the bottom they're looking for the key is can you produce

[00:26:23] credit score that's at least 620 ideally 640 let's say ideally higher for lower rates but

[00:26:28] just to get approved can you produce a credit score that's 620 that's what they ask first

[00:26:35] second they want to make sure that you have enough money to pay for whatever home that

[00:26:39] you're trying to do but the credit score just says can we even make a dang deal

[00:26:44] the money tells them how much home can you afford are you going to have enough money to

[00:26:50] be able to close it answers other questions about getting it done not necessarily the

[00:26:55] approval although it matters I'm not suggesting it doesn't I'm saying that it's kind of in

[00:26:59] that order the credit score is usually number one in the way they assess getting you know

[00:27:05] making a loan but the money is the key for your so-called buying power once you get past

[00:27:11] the credit score so let's take it on face and I'm not attributing this to everybody

[00:27:16] but let's take it on face that the vast majority of people are coming in with a 620 credit score

[00:27:22] bottom if you've been renting for a while if you don't use a lot of credit cards or if you do

[00:27:30] you pay them off if you have a car loan and you don't miss payments on your car loan

[00:27:35] if you have student loans that you pay on or are not in repayment and right now there's

[00:27:40] options for you not to be in repayment if for the most part your stuff's getting paid

[00:27:46] chances are you have a 620 credit score higher not guaranteed there's a lot of other conditions

[00:27:52] to what I just said but chances are you probably have a minimum 620 you can't pull your own

[00:27:57] credit score to know that this is why I said it's all going to come connected because of

[00:28:02] what I'm describing there's different scores depending on who's pulling it the score you

[00:28:08] pull for yourself is not the same score that the car dealership will get that score is not

[00:28:14] the same score that the mortgage company is going to get that score is not going to be the

[00:28:19] same as the credit card company is going to get the factors as it's described they're looking

[00:28:24] for different things that generate a different score because certain things are weighed more

[00:28:31] seriously than others bankruptcy is always severe it's always bad if you filed but the bankruptcy

[00:28:37] only stays for a certain number of years if you've missed payments on a home your mortgage

[00:28:43] company is going to care a hell of a lot more than the credit card company will a credit card

[00:28:48] cares if you missed hardly at most anything they care about inquiries there's certain things they

[00:28:51] care about then there's certain things they care about less like your car payments they don't

[00:28:55] care as much they care but not as much as your car company the car dealership would care

[00:29:01] the car dealer almost to a t they'll make a deal they'll get you in a car they'll make it

[00:29:09] it's just that the rate goes sky high you'll end up with a 20 plus percent rate so you're paying

[00:29:14] out the nose for that car for endless years which essentially is burning money if you think

[00:29:19] about it especially if you have a car that does not appreciate or depreciates at a more

[00:29:24] rapid pace than others which happens in the mortgage situation then if you can come in

[00:29:30] with a 620 credit score they're going to call out here's the factors that drop the score

[00:29:35] here's the things that we saw that lowered the score doesn't mean we can't work with you

[00:29:40] it means it lowered the score where the lower score comes a higher rate the higher rate is

[00:29:45] a bit painful but it really only matters based on the amount of home that you're trying to buy

[00:29:50] if you said you know what in my area i just need a little condo or something because it's

[00:29:56] just me and you know a spouse or something right now we need like a hundred thousand

[00:30:00] dollar condo but you may together you know ninety thousand dollars you can pull it off

[00:30:05] and so think about does that make sense to try to make that happen or does it make sense to

[00:30:11] stay renting nobody can tell you the right answer i'm saying that credit is no longer the

[00:30:16] barrier that you might think it probably was and likely was it's really now about the money

[00:30:23] saving saving up for this and considering that transaction as an investment when you rent

[00:30:32] that money's not invested for you they're doing things like rent track that's designed

[00:30:37] to benefit you on the credit report it doesn't really it really doesn't utility bills don't

[00:30:43] benefit you on the credit it really doesn't if you can purchase something it becomes an asset

[00:30:48] for you as an asset it extends other opportunities for you as you build equity that's other assets

[00:30:56] for you net worth is an asset for you these are things that can help you especially if you do

[00:31:01] have credit cards of course i don't but if you do and you can pay on the home you can use

[00:31:07] that in lieu of credit cards or use it to help pay off credit cards it opens up opportunities

[00:31:13] for you that you don't have when you're renting but it all starts with the question can you walk

[00:31:19] in there to whatever bank and i would recommend one of the smaller ones not the bigger ones but

[00:31:24] i've had situations with chase one of the largest that said yeah no problem and my credit

[00:31:29] wasn't stellar at the time so it's not just the small ones it's just that the smaller ones

[00:31:35] are more willing to work around any issues they find and then of course fha is there to help

[00:31:39] you you know if you're not able to make it work on the conventional lending let's talk about those

[00:31:44] loan programs with fha and with certain state programs that i'll recommend you avoid unless

[00:31:51] you have to their goal is to lend money they want more people to be homeowners that's their

[00:31:59] goal that's their purpose you have to be careful because if you're not coming in there

[00:32:03] with 20 down they attach what's referred to as mortgage insurance mortgage insurance is

[00:32:09] a misnomer because it doesn't really ensure anything think of it as a form of social

[00:32:14] security for the home market you're paying into a fund that's used to help other homes

[00:32:20] that might go to foreclosure that's essentially what you're doing so they'll tack on an extra

[00:32:24] couple hundred bucks or whatever to your mortgage payment in exchange for not having

[00:32:30] to have 20 down not having to have the full percent some state programs will offer down payment

[00:32:36] assistance they'll offer closing credits some sellers will offer closing credits there's all

[00:32:41] sorts of opportunities for you to offset the money part of a thing if you accept what i'm

[00:32:47] saying and you can research it and i encourage you do it tells you that the money is the key

[00:32:51] the money is all they really want to make sure happens everything else can be worked around

[00:32:57] the money there's multiple ways to deal with it this is not to suggest it's easy simply that

[00:33:03] there's a lot of programs more than you might think there are programs that are enticing people

[00:33:08] to purchase in certain counties that you might not want to live in but if you work from home

[00:33:12] what's the problem right and they'll pay they'll pay down payment assistance they'll pay

[00:33:17] closing credit assistance they'll do all sorts of stuff because they want more people buying

[00:33:22] homes in those areas the downside is by taking those programs you're acknowledging to the

[00:33:29] governments the local governments that you're not capable of paying it on your own and so then

[00:33:33] the rate goes higher because you are a risk because chances are you're going to foreclose

[00:33:40] if you're renting right now and you're happy renting continue renting this is not a sales

[00:33:45] pitch i'm describing to you the power of money now that wasn't always there before

[00:33:52] and the power of putting 20 down should you choose to buy is to offset other expenses that

[00:33:58] you don't see but also the strength of if you can buy the strength of those assets adding to

[00:34:04] your net worth and helping to grow your situation you might not realize it's actually

[00:34:10] easier than you think i would argue and you might shake your head and that's cool

[00:34:16] i would argue see a car dealer will sell you a car no matter what they'll figure it out i've

[00:34:22] never had a situation where i was denied the ability to buy a car it was always you can take

[00:34:28] this car but the rate's going to be sky freaking high or just don't take the car i've

[00:34:32] never had a situation where i was denied for a car ever so as interesting as it is

[00:34:40] this financial situation i say credit's a scam and have done and the reason i've done that is because

[00:34:48] credit by its very nature is used as a predatory tool if you have high credit scores

[00:34:59] it means that you're just you're following the system you're doing what the system wants you to

[00:35:04] do you're taking out credit so you're taking out loans you're taking out credit cards you're buying

[00:35:09] cars you're doing credit and you're making payments and they don't want you to pay too fast

[00:35:15] they don't want you to overpay they want you to do steady money flow for them and in exchange

[00:35:22] they tell the credit bureaus who are in the pocket of these orgs to go ahead and give them

[00:35:27] a numeric score that tells other lending institutions hey this person's a sucker and

[00:35:32] they're willing to pay you streams of money over time the truth is just because you have a high

[00:35:38] credit score does not necessarily mean that you're going to pay this company back things

[00:35:43] happen during covid the government didn't step in and say no you're not going to be allowed

[00:35:49] to ding people's credit due to factors outside their control they allowed these organizations

[00:35:55] to damage your credit at will and didn't think twice about it meanwhile people who continually

[00:36:01] paid their bills during covid what do they have to really show for it all they really have to

[00:36:06] show for it is they already have those loans they already have those homes they already have

[00:36:10] those cars so they don't really need the score when i say credit's a scam i'm saying that

[00:36:18] the whole concept of punishing somebody for something outside of your control is a scam

[00:36:26] i'm saying that enriching somebody with a high credit score that doesn't really need

[00:36:31] the enrichment is a scam it's a separation of wealth and all the while there's only one

[00:36:39] difference between a higher credit score and a lower credit score and that's if you have a

[00:36:45] lower credit score it's more punitive against you it's more predatory against you that's why

[00:36:51] it's a scam it's designed to take advantage of you to encourage you to play by their rules

[00:36:58] and that's fine if you choose to do it this isn't saying don't i'm explaining why leister

[00:37:05] is said says it's a scam it's a scam because the whole point is to get you to fall in line

[00:37:11] with what they want which is recurrent income if you're the kind of person who makes a lot

[00:37:16] of money on your job to the point that you don't need credit you don't take credit cards

[00:37:23] you pay cash for cars you refuse to take out loans but you pay cash for everything

[00:37:30] they don't the system doesn't like you the system doesn't like you because it's not recurrent

[00:37:35] income it's not steady streams of income that they're bleeding from you so they don't reward

[00:37:41] you for being financially diligent they don't want people like you they want people who are

[00:37:49] willing to be saddled to a system and constantly streaming money over to them

[00:37:55] so they can collect that interest over time and so that they can bank on it it's basically house

[00:38:00] of cards they can bank on streams of income years and years and years and years and years

[00:38:04] so they reward you by the way of a high credit score and that score is simply used

[00:38:08] to attract other lenders and banks to do the same thing and exploit you that's why it's a

[00:38:13] scam if you buy a home with a high credit 780 let's say credit score which is very shy of the

[00:38:21] highest you can get you're going to get the best interest rates possible very low interest rates

[00:38:27] but consider if you come in with a 620 credit score you get a higher rate perhaps the only

[00:38:35] reason you have a low credit score is because you chose not to do any credit cards

[00:38:40] because you were too busy saving to buy a home and you didn't think it would make any sense

[00:38:45] to extend new credit because extending new credit drops your credit score applying for

[00:38:51] credit drops your credit score do you understand this is the scam going after said credit

[00:39:00] is a putt you're punished for this not going after it you're punished for it

[00:39:05] it only benefits certain segments of the audience who don't need it in the first place

[00:39:12] that's who it benefits and the rates that they get are offset by the fact that they're going to

[00:39:17] get punished by the way you're just applied for a new loan so we're gonna drop your credit

[00:39:24] score because of the inquiry that comes into credit score it doesn't last for more than

[00:39:28] a couple years but the point is it punishes you for even applying so you can't win

[00:39:33] so you can't win other than you didn't need it and you don't go after it that is why the

[00:39:40] wealthy generally have bad credit because they don't bother they just pay cash and say screw it

[00:39:45] i'm not going to go with the system some wealthy who are no longer wealthy take out loans

[00:39:51] to offset the outbound spend because they're creating their own house of cards but what

[00:39:55] happens when that money starts flowing in there now your their their credit agencies

[00:40:00] are not going to cut you a break they're going to tank your credit like nothing and it's a lot

[00:40:05] harder to build your credit up than it is to allow it to drop your credit can drop hundreds

[00:40:09] of points with one mistake and that happened during covid to a lot of people so in summary

[00:40:16] if you're considering buying a home or if you're not and hadn't thought about it till

[00:40:20] you heard the show all i'm saying is credit's a scam because it's it's slanted towards people

[00:40:27] who don't need it if you're at the point that you're considering buying a home after not being

[00:40:33] sure that you can afford it chances are your credit's not up to snuff but you can still buy

[00:40:38] a home because the credit programs by and large are looking for a reasonably low score it's not

[00:40:43] doesn't have to be crazy high to get into a home but you're going to be nailed on the

[00:40:47] interest which means your buying power that should be lower you know consider a lower home

[00:40:53] price don't go all in the downside is of course security safety schools crime you know things that

[00:41:00] you i'll have to compromise if you choose to do it or stay renting understanding that the rent

[00:41:06] money is going in a black hole it's not benefiting you directly later after you buy

[00:41:12] a home you're going to see your credit score just start to go up as you make payments on

[00:41:17] that house your credit score is going to score credit score is going to start skyrocketing

[00:41:22] because the other factor to this that i didn't talk about is diversity of credit if you have a

[00:41:29] credit card let's say you only have the one let's say you have one loan and then you get

[00:41:33] this mortgage the diversity of types of credit are actually calculated in the score factors

[00:41:41] so what does that mean that means that people who have never bought a home

[00:41:44] and hadn't planned to can never have a credit score close to somebody who does have

[00:41:49] a home who did have a home loan this ties back to shadows of the past people that are older

[00:41:59] who were able to get into those homes who were able to get into those programs when homes were

[00:42:04] cheap and then generate you know generational wealth later and we know that a segment of

[00:42:10] the audience was not able to do that so then credit scores it's a glass ceiling you could

[00:42:15] never get past a certain level no matter how good your credit card payment history was

[00:42:20] it didn't matter because one of the factors is do you have different types of accounts age

[00:42:26] of accounts is a factor that plays in if you're a 20 something or a 30 something

[00:42:31] who got your credit card you know not that long after you graduated high school

[00:42:37] you don't have enough quote age of the account and even then the age doesn't play

[00:42:42] significant of a factor positive compared to how much negative an inquiry is it's all a game

[00:42:50] and it's all a scam the key is can you use it to your advantage buying a home when you're ready

[00:42:58] is a way to put it to your advantage it just when are you ready to do it

[00:43:03] and i'm stressing that the money is the key to being able to do it less so than the credit

[00:43:10] less so the credit so if you can get enough money to make it make sense you can offset

[00:43:16] the credit expectations it doesn't make them go away but think about it if you're trying

[00:43:21] to get something that's a you know i don't know where you live but let's say you can

[00:43:24] get something for 100 grand little condo or something instead of an apartment for 100 grand

[00:43:30] 20 percent of that's what 20 grand okay so can you save up 20 000 dollars to put on

[00:43:36] that to get it in there and then your monthly payments i guarantee you're going to be lower than

[00:43:40] your rent payment and if you can do that that builds up an asset for you you build up equity

[00:43:47] in it you're in something that you own something that benefits you directly you take on more

[00:43:52] expenses in some cases because some of the utilities might have been paid before by the

[00:43:57] apartment complex and so you do need to balance that out but if you can do that

[00:44:01] you're building in assets and equity and you can use some of that equity at some point

[00:44:06] to grow your credit profile and to consider other purchases right if you're trying to up

[00:44:13] let's say you're building a family you know you can buy something larger once you have enough

[00:44:18] equity in the home a sell it spins go something else just to start somewhere one thing i wish i

[00:44:24] had done i didn't but i wish i had done is to sell the home that i had in washington state

[00:44:31] and use that to then buy a different house somewhere else that was not

[00:44:36] colorado i didn't do it because i wasn't sure i would be able to and perhaps i wouldn't have

[00:44:42] been able to but i should have at least tried and i didn't try but if i had tried

[00:44:47] because it was an asset i owned it it was my house but if i had tried who knows what might

[00:44:52] have happened as a result where i wouldn't have had to have as much struggle during the pandemic

[00:44:57] because i would have had that asset in the back pocket if i had still had my home during

[00:45:02] the pandemic it wouldn't have been as hard because part of the reason that it was a struggle

[00:45:07] is i was renting and with rent they want it when they want it talking about money with a

[00:45:12] house you kind of have a couple months to play around a little bit before they you know

[00:45:16] have to you know shut down the house so hopefully that's beneficial and clarifies why i say credit

[00:45:23] is a scam it's a scam because it's slanted towards people who don't really need it

[00:45:28] and it's designed to benefit certain people we're talking lines of wealth benefit certain

[00:45:33] people at the expense of other people it doesn't mean it doesn't matter i am saying that when

[00:45:39] you're going to buy a home i think that money matters a lot more than you think that it

[00:45:45] should it certainly matters more than credit um the way it used to be the way it used to be was

[00:45:53] if the credit was toast it didn't matter how much money you came but i think it's getting

[00:45:58] they're starting to understand it's harder for people to get these high freaking credit

[00:46:02] scores so they're just offering better rates but it's no longer a closed door and that may

[00:46:07] create an opportunity for somebody who might be interested in doing that